Why Stablecoins Are Becoming the Default Payment Rail in 2026

Stablecoins enable instant, low-cost, 24/7 payments, driving bank, merchant, payroll, and remittance adoption worldwide.

Stablecoins are now the preferred way to move money globally in 2026. Here's why:

- Transaction Volume: In 2025, stablecoins processed $46 trillion - three times Visa's volume.

- Speed & Cost: Transactions settle in seconds and cost fractions of a cent, unlike traditional systems that take days and charge high fees.

- Regulatory Clarity: The 2025 GENIUS Act provided clear rules, boosting confidence among banks and businesses.

- Adoption by Major Players: Visa, Stripe, and others now support stablecoin payments, making them accessible worldwide.

- Global Use Cases: From payroll to retail purchases and remittances, stablecoins are integrated into everyday financial activities.

Stablecoins are reshaping payments by combining the stability of the dollar with the efficiency of blockchain. They’re faster, cheaper, and available 24/7, making them a practical alternative to older systems.

Benefits of Stablecoins Compared to Standard Payment Systems

Stablecoins vs Traditional Payments: Speed, Cost, and Accessibility Comparison

Stablecoins bring tangible economic benefits to both businesses and individuals. Unlike traditional payment systems, which function as messaging networks where banks promise to settle later, stablecoins are digital assets that transfer value instantly. This fundamental shift is changing how payments are made and received.

Stablecoins vs. Standard Payments: A Comparison

Here’s a quick look at how stablecoins stack up against traditional payment systems:

| Feature | Traditional Fiat (Cards/SWIFT) | Stablecoin Payments (USDC/USDT) |

|---|---|---|

| Settlement Speed | 1–5 Business Days | Instant (Seconds to Minutes) |

| Transaction Fees | 1.5%–3.5% + FX Fees | Low Fixed Fee (often <$0.01) |

| Availability | Banking Hours (Closed Weekends) | 24/7/365 (Always On) |

| Chargeback Risk | High (Reversible for months) | Zero (Final/Irreversible) |

| Intermediaries | Multiple (Issuers, Acquirers, Networks) | None (Direct Peer-to-Peer) |

| Accessibility | Requires Bank Account/Credit Approval | Requires only Smartphone/Wallet |

Data Sources: for technical features; for accessibility criteria.

Lower Costs and Faster Transactions

The cost difference between traditional payments and stablecoin transactions is hard to ignore. For example, international transfers typically come with fees exceeding 6%, which means sending $200 could cost over $12 in fees. Stablecoins, on the other hand, can process transactions for fractions of a cent on networks like Solana or Polygon. For businesses handling large volumes, this translates into billions in potential savings by moving away from traditional card fees (1.5%–3.5%) to stablecoin processing costs as low as 0.1%.

Speed is another game-changer. Traditional SWIFT transfers take 2–5 business days and are often delayed by weekends or holidays. Stablecoins bypass these delays, settling transactions in seconds to minutes. In October 2024, Stripe made waves by acquiring Bridge.xyz for $1 billion and rolling out stablecoin payment options with a 1.5% merchant fee - a 30% reduction compared to standard card processing costs. Companies adopting stablecoins have reported up to 71% in cost savings and a 40% boost in working capital efficiency.

"Stablecoins offer transformative capabilities that address key limitations of legacy payment systems, such as increased speed; lower costs; borderless, minimal, or nonexistent foreign transaction fees; and 24/7 operations", McKinsey & Company noted.

These advantages go beyond just saving money - they also pave the way for greater financial inclusion.

Expanding Access for Underserved Communities

Stablecoins don’t just make payments cheaper and faster; they also open doors for people who have been excluded from traditional financial systems. Over 1 billion unbanked individuals worldwide now have access to financial tools through stablecoins, requiring only a smartphone and Internet connection. This is especially impactful in regions like Africa, South America, and Asia, where stablecoins act as essential financial infrastructure rather than speculative assets.

sbb-itb-0796ce6

How Stablecoins Are Being Used Today

Stablecoins have transitioned from being a theoretical concept to becoming a practical tool in daily life. By late 2025, businesses were processing more than $10 billion monthly in stablecoin payments for goods and services. This growing adoption highlights their importance in modern digital payments.

Business Payments and Employee Payroll

Ripple's payment platform, as of April 2025, had handled $70 billion in total volume across over 90 payout markets. Companies like BKK Forex and iSend have been using the platform to settle cross-border transactions instantly, avoiding the delays associated with traditional banking systems. Business-to-business (B2B) stablecoin payments have grown to $36 billion annually, and 25% of global businesses now use cryptocurrency for payroll.

The "stablecoin sandwich" model has emerged as a popular method for transfers. Here’s how it works: the sender funds a transfer in their local currency, the provider converts it to a stablecoin for fast blockchain transit, and the recipient receives payment in their local currency. This approach eliminates concerns about crypto volatility while offering speed and cost efficiency. Businesses typically use one of three payroll models:

- Invoice-to-Stablecoin: Ideal for contractors.

- Hybrid: Combines a fiat base salary with stablecoin bonuses.

- Treasury-style: Maintains a stablecoin reserve for scheduled payouts.

Among businesses using stablecoins, 63% prefer USDC due to its regulatory clarity and backing by institutions. These payroll innovations are setting the stage for expanded retail and cross-border use cases.

Store Purchases and Merchant Adoption

Retailers are increasingly accepting stablecoins at checkout to reduce costs and speed up payment settlement. By February 2026, crypto-linked cards were facilitating over $1.5 billion in monthly payment flows. Platforms like Shopify and Stripe now support USDC natively, enabling millions of merchants to accept stablecoin payments through their existing systems. Visa, in December 2025, reported $1.23 trillion in stablecoin transaction volume.

For merchants, stablecoin transactions offer significant savings. Traditional payment processing fees typically range from 2% to 7%, but stablecoin fees can be as low as 0.5%, sometimes costing just fractions of a cent. A 2025 survey revealed that 52% of corporate executives were drawn to stablecoins primarily to lower transaction costs. Transactions settle in under 60 seconds, are final upon confirmation, and eliminate chargeback risks. For those wary of volatility, services like Stripe and BitPay offer automatic conversion of stablecoins to fiat currency for bank deposits, providing added convenience.

International Money Transfers

Stablecoins are also transforming international remittances. By January 2026, Circle reported its USDC stablecoin had surpassed $55 trillion in lifetime trading volume. Retail usage for small-value transfers (under $250) hit $5.84 billion in August 2025, showcasing a growing reliance on stablecoins for everyday remittances.

Compared to traditional methods, stablecoin transfers are far more cost-effective. In 2025, fees for conventional remittances averaged over 6%, far exceeding the G20's 1% target, with hidden foreign exchange spreads adding another 5%. Stablecoin transfers, on the other hand, often cost only a few cents and settle within minutes, regardless of banking hours. In late 2025, Visa introduced live USDC settlements with U.S. banks, enabling instant on-chain payments and allowing merchants to receive funds around the clock, bypassing delays linked to traditional banking systems.

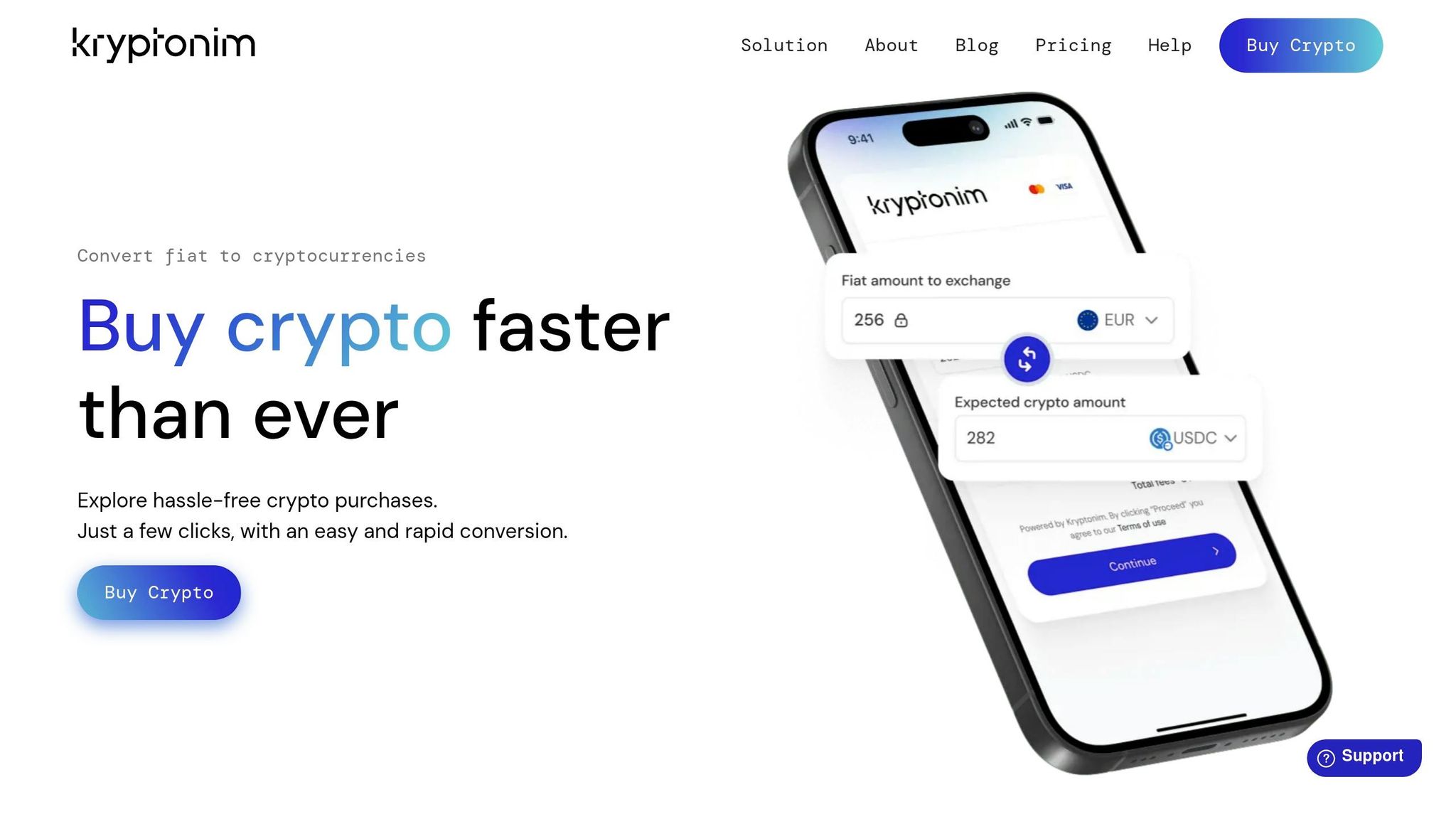

How to Start Using Stablecoins on Kryptonim

Stablecoins are changing the way global payments work, and Kryptonim makes it easy for anyone to get started. Whether you're new to cryptocurrency or just looking for a seamless way to spend your digital assets, Kryptonim removes the technical hassles while ensuring top-notch security and compliance as an EU-regulated exchange.

Buying Stablecoins on Kryptonim

Kryptonim keeps it simple. You can make basic stablecoin purchases without even creating an account. However, completing the verification process opens up additional features, including getting a virtual card issued shortly after approval. The platform supports local payment methods and offers transparent pricing: 2% fees for EU transactions and 4% for non-EU transactions - no hidden charges.

Once you buy stablecoins like USDC, they’re ready for immediate use. Kryptonim’s wallet takes care of the technical details, so you don’t have to. This streamlined process ensures your stablecoins are available for spending or transferring right away, making it a cost-efficient and quick solution for managing digital assets.

After your purchase, Kryptonim’s payment features allow you to start using your stablecoins instantly.

Making Payments with Kryptonim

Spending your stablecoins is just as easy. Kryptonim offers a Visa-branded payment card that lets you use stablecoins anywhere Visa is accepted. Whether it’s for groceries, travel, or subscription services, the card automatically converts your stablecoins into fiat currency at checkout. This means merchants receive traditional money, and you don’t have to worry about whether they accept crypto.

For those who prefer mobile payments, the Kryptonim Card integrates seamlessly with Google Pay. This allows for secure, one-tap payments in stores. Plus, the virtual card comes with no monthly fees, making it a budget-friendly option for everyday use.

Chris Harmse, Co-Founder & Chief Business Officer at BVNK, summed it up well: "Users want stablecoin payments to feel normal: universal acceptance, simple UX, and built-in security".

This aligns with broader trends. A recent survey revealed that 71% of stablecoin holders are inclined to use a card for spending, and 50% actively choose businesses that accept stablecoins. Kryptonim’s features make stablecoins a practical and reliable option for daily transactions.

| Feature | Details |

|---|---|

| Virtual Card Fee | $0.00/month |

| Merchant Acceptance | Anywhere Visa is accepted |

| Mobile Wallet Support | Google Pay integration |

| Conversion | Automatic at point of payment |

| EU Transaction Fee | 2% per transaction |

| Non-EU Transaction Fee | 4% per transaction |

What's Next for Stablecoins in Payment Systems

Stablecoins are no longer just a niche tool for crypto enthusiasts - they're rapidly becoming a cornerstone of global finance. By 2025, stablecoin transaction volumes are projected to hit $33 trillion, a 72% jump from the previous year, signaling their growing importance in everything from business payments to payroll and merchant transactions. What began as a tool for crypto traders is now evolving into a critical infrastructure for global commerce, with banks, regulators, and businesses driving their adoption. This momentum is setting the stage for new blockchain-powered capabilities that traditional financial systems simply can't match.

Stablecoins and New Financial Technologies

Blockchain technology is unlocking possibilities that were unimaginable with older payment systems. One of the most exciting developments is programmable settlement. Stablecoins can now include built-in instructions, automating processes like escrow releases, revenue sharing, or milestone-based payments - all without manual intervention. For example, in 2025, Stripe processed $400 billion in stablecoin payments, with 60% of those transactions coming from B2B use cases. Businesses are leveraging stablecoins as "programmable settlement containers", integrating them directly into accounting platforms, treasury systems, and other financial tools. This flexibility allows stablecoins to function across various blockchains and interact with tokenized assets, creating a seamless payment layer that traditional systems can't replicate.

"Instead of using checks and wires, businesses will settle an increasing number of payments with stablecoins. The main advantage will be speed and finality of settlement", explains Fred Krueger, an industry analyst.

The market is also evolving into two distinct tiers: regulated onshore stablecoins for institutions and corporations, and offshore liquidity stablecoins designed for fast global transfers. This division lets users choose between compliance-focused solutions for corporate needs or faster, less restrictive options for international payments.

Adoption by Banks and Governments

As the technology advances, banks and governments are fully embracing stablecoins. In December 2025, 10 major European banks, including ING and BNP Paribas, formed qivalis to launch a euro-backed stablecoin compliant with MiCA regulations, set to debut in the second half of 2026. Around the same time, Société Générale's SG-FORGE introduced USD CoinVertible (USDCV), a dollar-backed stablecoin operating on Ethereum and Solana, with BNY Mellon managing its reserves. These initiatives show how institutions managing trillions of dollars are building stablecoin-ready payment systems.

Regulatory clarity is also driving adoption. Laws like the US GENIUS Act and the EU's Markets in Crypto-Assets (MiCA) now require stablecoins to maintain 1:1 reserve backing with high-quality assets such as cash and Treasury bills. Analysts predict that by 2030, these regulations could channel over $1.9 trillion into U.S. Treasury purchases.

"The GENIUS Act is a big step forward for stablecoins, giving them the recognition as the link between traditional finance and digital assets", says Luis Ferreira, Commercial Director VASP at Bank of London.

Card networks are also jumping on board. In March 2026, Visa announced the expansion of its stablecoin-linked card program to over 100 countries, following successful trials in Latin America. Similarly, Pine Labs launched a prepaid card backed by stablecoins across nine countries in the Middle East, Africa, and Southeast Asia, enabling users to spend stablecoin balances with instant local currency conversion. These developments highlight how stablecoins are becoming an integral part of financial infrastructure, enabling instant settlement for users while merchants receive traditional currencies.

"There is a clear 4–5 year opportunity window during which stablecoins could dominate the market and capture significant adoption before EU CBDCs reach production", notes Lucian Mincu, Co-founder of MultiversX Labs.

With $500 billion expected to shift from bank deposits to stablecoins by 2028, the financial system is undergoing a major transformation in real time.

Conclusion

Stablecoins have become a key part of modern payment systems, enabling everything from payroll processing to cross-border invoicing. The numbers tell the story: by 2025, transaction volumes hit $46 trillion, with the total supply surpassing $300 billion. This growth stems from stablecoins addressing challenges that traditional payment systems struggle with - offering features like 24/7 availability, ultra-low transaction costs, and secure, irreversible payments that eliminate chargebacks and delays.

A major turning point came in July 2025 with the passage of the GENIUS Act, which provided a clear regulatory framework for institutional use of stablecoins. The response was immediate - companies like Visa, Stripe, and European banks built infrastructure capable of processing hundreds of billions of dollars in stablecoin payments annually. For businesses, this meant replacing outdated and costly correspondent banking systems with instant, transparent settlements. For consumers, the shift is seamless: whether tapping a card or scanning a QR code, stablecoins quietly power these transactions behind the scenes.

"The first wave of stablecoin innovation and scaling will really happen in 2026", notes Chris McGee, Global Head of Financial Services Consulting at AArete.

Looking ahead, the stablecoin market is projected to reach $4 trillion by 2030. The infrastructure being developed today is paving the way for programmable money capable of automating processes like escrow, revenue sharing, and milestone payments - no human intervention required. Interestingly, banks are not resisting this change; they’re actively building the systems to support it. Since 2020, stablecoins have reshaped the foundation of digital payments, and their role as the backbone of the financial ecosystem continues to expand.

FAQs

Are stablecoin payments safe if a company fails?

Stablecoin payments aren't without their risks, especially if the issuer encounters financial trouble or insolvency. These digital currencies depend on backing assets, meaning any doubts about the issuer's reserves or stability can shake confidence. While stablecoins come with plenty of benefits, being aware of these possible weaknesses is crucial when considering them for payments.

What fees or taxes do I pay when spending stablecoins?

When using stablecoins for transactions, network fees are generally quite low, often ranging from $0.002 to $0.01 per transaction. However, some platforms might include an additional processing fee of around 1.5%. On top of that, you may also encounter taxes or regulatory fees, which vary based on your local laws. It's important to review the regulations in your area to ensure you're aware of any applicable charges.

How do I start using stablecoins for everyday purchases on Kryptonim?

To start using stablecoins for everyday purchases on Kryptonim, begin by setting up a compatible wallet to safely store your stablecoins. Once your wallet is ready, fund it through an exchange or by transferring stablecoins from another source. Next, link your wallet to Kryptonim’s platform or any merchant that accepts stablecoins. At checkout, choose stablecoins as your payment method and approve the transaction. For extra ease, you might want to explore stablecoin payment cards if the option is available.