How Gen Z Is Using Stablecoin Apps Instead of Bank Transfers

Gen Z is ditching banks for stablecoin apps that deliver instant, low-fee, 24/7 peer-to-peer and cross-border payments.

Gen Z is ditching bank transfers for stablecoin apps. Why? These apps offer faster, cheaper, and more efficient money transfers, aligning perfectly with their mobile-first lifestyle. Here’s what you need to know:

- Speed: Transfers settle in seconds, unlike the 2–5 business days it takes for banks.

- Cost: Fees are minimal - often just pennies - compared to the 1.5%–6.6% average for banks.

- Access: Available 24/7, no downtime, and no need for a traditional bank account.

- Trust: While only 22% of Gen Z trusts crypto more than banks, that’s still a significant shift compared to older generations.

Stablecoin apps like Kryptonim are gaining traction by simplifying the process: user-friendly interfaces, reduced fees, and real-world payment options like bills and salaries. With 75% of Gen Z open to receiving paychecks in stablecoins, this shift represents a generational change in how money moves.

Main Features of Stablecoin Apps Gen Z Uses

Stablecoin apps are gaining traction with Gen Z by offering sleek designs and instant, affordable transfers. These apps cater to a generation that values quick, accessible, and cost-effective financial tools.

Easy to Use and Access

Cryptocurrency adoption used to be hindered by technical barriers - think complex wallet addresses, seed phrases, and jargon-heavy interfaces. Today’s stablecoin apps have simplified the experience. Instead of dealing with long strings of characters, users can send and receive funds using easy, human-readable usernames like @username. Plus, topping up wallets is as simple as using Apple Pay or Google Pay.

Another user-friendly feature is the automation of network fees, so users aren’t hit with unexpected blockchain costs. For instance, a user in Argentina shared that they complete 10–15 tasks daily and receive payments almost instantly.

Lower Fees and Faster Transactions

Cost and speed are where stablecoin apps truly shine. Traditional bank transfers can be expensive and slow. In 2023, global remittance fees averaged 6.62%, and nearly half of all cross-border payments took over 24 hours to process. Stablecoin apps flip the script, charging just pennies - or even fractions of a cent - per transaction. Networks like Solana, for example, can process a transaction in as little as 400 milliseconds. And unlike banks, which operate on limited hours, blockchain networks run 24/7/365.

For businesses and freelancers, the savings are substantial. Some platforms report helping users cut cross-border payment costs by 35% using USDC and blockchain technology. Meanwhile, nearly 48% of freelancers have faced delays of three or more days when using traditional international payment methods.

Here’s a quick comparison:

| Feature | Traditional Bank Transfers | Stablecoin Apps |

|---|---|---|

| Settlement Time | 1–5 business days | Seconds to minutes |

| Availability | Banking hours (Mon–Fri) | 24/7/365 |

| Average Fees | 1.5%–6.6% | Pennies or zero |

| Intermediaries | Multiple correspondent banks | None (peer-to-peer) |

| Transparency | Pending status | Real-time (on-chain) |

The numbers back up these advantages. As of January 14, 2026, the stablecoin market cap surpassed $300 billion - a 55% increase compared to the previous year. Small-value transfers under $250 also hit a record $5.84 billion in August 2025.

Peer-to-Peer and International Payment Support

Beyond affordability and speed, stablecoin apps excel at facilitating seamless peer-to-peer and international payments. Whether you’re sending money to a friend nearby or across the globe, transactions happen instantly and cost far less than traditional methods.

Some apps even let users pay real-world bills directly from their wallets. For example, U.S. residents can use USDC to pay for mortgages, utility bills, or student loans - no need to convert to fiat currency first. Over 80% of these payments are made using USDC, backed by security features like Two-Factor Authentication and soft credit checks.

For international transactions, stablecoins eliminate the need for intermediary banks, which often add delays and fees. It’s no wonder that 81% of freelancers expressed interest in stablecoin payouts, citing their speed and security.

How to Use Kryptonim for Stablecoin Transactions

Kryptonim makes it simple to buy and send stablecoins without needing a full account. As an EU-regulated fiat-to-crypto onramp, it converts currencies like dollars into stablecoins such as USDC, USDT, PYUSD, DAI, and USDE with minimal hassle. To get started, all you need is an email address. If you're in the U.S., U.K., or Canada, you'll also need to provide a billing address. Here's a guide to help you navigate the process.

Step-by-Step Guide to Buying Stablecoins on Kryptonim

- Visit the Kryptonim website and access the converter tool.

- Choose your stablecoin and enter an amount (minimum $10).

- Select your payment method: Options include cards, Apple Pay, or Google Pay, which typically process in 2–20 minutes. Volt bank transfers (EUR only) may take up to 3 days.

- Provide your wallet address: Kryptonim doesn’t offer a built-in wallet, so you’ll need to use a trusted third-party wallet like MetaMask or Trust Wallet.

- Verify your identity: Complete the process using a valid ID and facial recognition, then confirm your payment.

Fees: EU users pay a 2% fee, while others pay 4%. Additional network fees may apply.

Sending Peer-to-Peer Transfers with Kryptonim

Once you’ve acquired stablecoins, sending them is equally straightforward:

- Open your wallet app and select the "Send" option.

- Enter the recipient’s wallet address or scan their QR code to avoid errors.

- Confirm the transaction is on the correct network (e.g., Ethereum, Polygon, Solana, or Arbitrum). Sending assets on an incompatible network can result in permanent loss.

- For first-time transfers, it’s a good idea to send a small test amount before transferring larger sums.

Most transfers are completed within minutes, and you can track confirmations on the blockchain. Network fees usually range from $1 to $10, though Ethereum fees may spike during periods of high activity.

Making International Payments with Kryptonim

Kryptonim supports over 27 fiat currencies, making it a practical choice for cross-border payments. The process mirrors how you buy stablecoins, but instead of entering your wallet address, you’ll provide the recipient’s.

For lower costs, consider using stablecoins on networks like Polygon or Arbitrum instead of Ethereum. While traditional international transfers can take 3–5 business days and cost 3–8% in fees, Kryptonim transactions are typically completed in 2–20 minutes and cost less than 1% of the transfer amount, offering an estimated 80–90% savings.

Since blockchain transactions can’t be reversed, always double-check the recipient’s wallet address before confirming the payment.

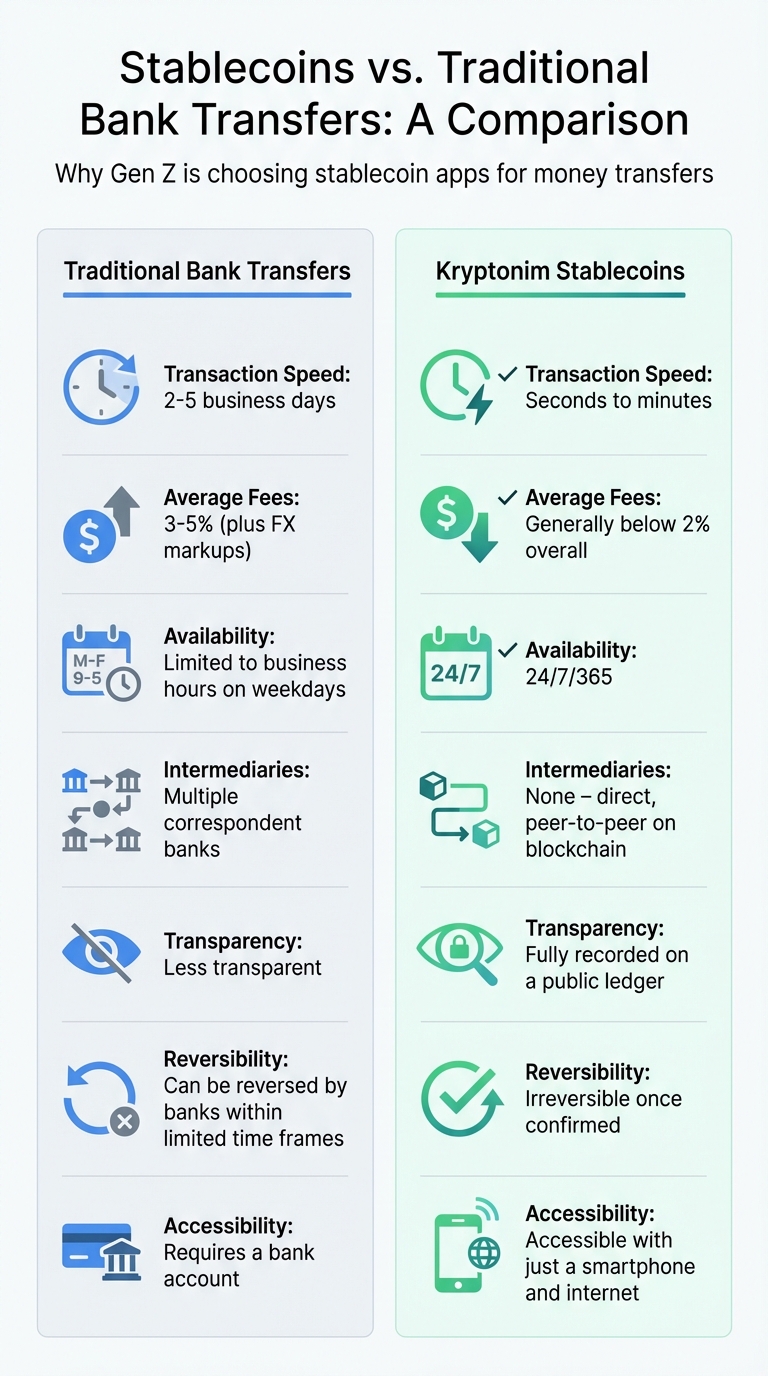

Stablecoins vs. Traditional Bank Transfers: A Comparison

Stablecoins vs Bank Transfers: Speed, Cost and Availability Comparison

Stablecoins offer a direct way to move funds on blockchain networks, cutting out the intermediaries typically involved in traditional banking systems like SWIFT and correspondent banks. This streamlined approach highlights how platforms like Kryptonim simplify transactions for today’s users.

One of the biggest advantages of stablecoins is transaction speed. With Kryptonim, stablecoin transfers settle in seconds or minutes, operating non-stop, 24/7/365. As Team Circle explains:

"Stablecoin transactions can settle in minutes (or seconds), not days. Running on blockchain rails, there are no payment cut‑off windows for non-standard operating hours, weekends, or holidays."

In contrast, traditional international bank transfers can take 2–5 business days to process. They also tend to be more expensive, with fees ranging from 3–5% (plus currency exchange markups). Kryptonim’s stablecoin transactions, on the other hand, typically cost less than 2% overall, offering a much more budget-friendly alternative.

Comparison Table: Kryptonim Stablecoins vs. Bank Transfers

For Gen Z users who value speed, affordability, and convenience, the differences outlined below are especially appealing.

| Feature | Traditional Bank Transfers | Kryptonim Stablecoins |

|---|---|---|

| Transaction Speed | 2–5 business days | Seconds to minutes |

| Average Fees | 3–5% (plus FX markups) | Generally below 2% overall |

| Availability | Limited to business hours on weekdays | 24/7/365 |

| Intermediaries | Multiple correspondent banks | None – direct, peer-to-peer on blockchain |

| Transparency | Less transparent | Fully recorded on a public ledger |

| Reversibility | Can be reversed by banks within limited time frames | Irreversible once confirmed |

| Accessibility | Requires a bank account | Accessible with just a smartphone and internet |

Another standout feature of stablecoins is transparency. Every transaction is permanently recorded on a public ledger, making it easy to verify and track. This level of openness contrasts sharply with the opaque processes often associated with traditional banking.

sbb-itb-0796ce6

Getting More Value from Kryptonim Stablecoins

Reducing Fees with Kryptonim

On top of offering faster transactions, Kryptonim helps users save money by cutting down on fees. With a straightforward pricing structure - 2% transaction fees for EU users and 4% for others - Kryptonim eliminates hidden charges like foreign exchange markups or extra bank fees. This transparency means more cash stays in your pocket.

The real game-changer lies in choosing the right networks. For instance, transferring stablecoins through networks like Solana or Polygon can bring transaction costs down to fractions of a cent - far lower than Ethereum's fees during busy periods. Families making regular international payments could save anywhere from $300 to $600 annually by switching to stablecoins.

If you're planning a big transfer, it’s smart to check current gas prices first. Stablecoins are also proving their worth for smaller, everyday transactions. In August 2025, payments under $250 using stablecoins hit a record $5.84 billion. This surge highlights their appeal for low-value, frequent payments.

By cutting fees, Kryptonim makes stablecoins a practical choice for everyday use, helping users save on routine transactions.

Using Stablecoins for Daily Transactions

The combination of lower fees and smooth transactions makes stablecoins ideal for day-to-day use. Gen Z, in particular, is finding creative ways to integrate them into their financial routines. With a Kryptonim wallet, you can pay bills - like utilities, credit cards, or loans - directly, avoiding the hassle and expense of converting stablecoins back to traditional currency.

Christopher Sheehan, the founder of Spritz, sums up this shift perfectly:

"Where most consumers think that they need to wait for banks and businesses to use cryptocurrency for transactions and payments, we saw another path to creating real-world financial utility for crypto."

The key strategy? Keep your assets on-chain as much as possible. Only convert funds when absolutely necessary for expenses that can’t be covered with stablecoins. This approach minimizes fees and ensures your money is always ready to use. With 75% of Gen Z open to receiving their paycheck in stablecoins, salaries can arrive instantly and be put to work immediately - no waiting for bank clearance.

For small payments or bill pay, stablecoins help you avoid flat fees and conversion costs. Just double-check that the recipient's wallet supports your chosen blockchain network to prevent any issues.

These everyday advantages make Kryptonim's stablecoins a cornerstone of Gen Z's growing digital economy.

Conclusion: Why Stablecoins Are Gen Z's Preferred Choice

Gen Z is skipping traditional banks in favor of faster, cheaper ways to move money. Platforms like Kryptonim offer exactly what this generation prioritizes: speed, low costs, and control. While bank transfers drag on for three to five business days, stablecoin transactions are lightning-fast - settling in under two minutes, and sometimes as quickly as 0.6 seconds on high-speed networks. It's no surprise that 75% of Gen Z would rather get paid in stablecoins than wait for bank processing times.

Cost is another major factor. Stablecoin transactions cost less than a cent, compared to the hefty 6% fees often tied to international bank transfers. For a generation where 53% already use stablecoins and 46% make monthly transactions, these savings are a big deal. On average, sending money internationally with stablecoins saves users 40% compared to traditional remittance services. But it’s not just about saving money - it’s about unlocking new possibilities.

Stablecoins go beyond simple payments. They’re programmable, global, and always available. This means Gen Z can instantly allocate their wages into savings, investments, or decentralized finance (DeFi) opportunities, all while keeping full control of their funds. With 71% of Gen Z ready to use stablecoins for everyday purchases and the market cap surpassing $300 billion as of January 2026, this isn’t just a passing trend - it’s a clear sign of where the future is headed.

FAQs

Are stablecoin transfers safe?

Stablecoin transfers are considered secure because they are tied to fiat currencies and operate on blockchain technology, which offers a high level of transparency. However, they’re not without risks. Issues like technological glitches or shifts in regulations can pose challenges. To stay protected, it's important to stay updated and thoroughly research before making any transactions.

What happens if I send to the wrong wallet or network?

When sending stablecoins, accuracy is everything. If you send them to the wrong wallet or use the wrong network, you might lose access to your funds permanently. Blockchain transactions are one-way and cannot be undone, so it’s essential to get it right the first time. Always double-check the wallet address and network details before hitting send. A few extra seconds of caution can save you from costly mistakes.

Do I have to pay taxes when using stablecoins?

Yes, the IRS classifies stablecoins as property. This means that actions like selling, trading, or using them for payments can trigger taxable events. Depending on the transaction, you might face capital gains or income taxes.