Checklist for Generating Crypto Tax Reports

Step-by-step checklist to gather crypto records, track income, calculate gains/losses, complete Form 8949/Schedule D, and file by April 15, 2026.

Crypto taxes can be overwhelming, but staying organized is key. The IRS treats cryptocurrency as property, meaning every sale, trade, or use triggers a taxable event. With new rules like Form 1099-DA and wallet-level cost basis tracking, accurate reporting is more important than ever. Here's a quick breakdown to help you prepare:

- Gather Records: Collect all transaction details (dates, amounts, fees, and fair market values) from exchanges, wallets, and platforms.

- Track Income: Record crypto income from staking, mining, airdrops, or services, including fair market values at receipt.

- Identify Taxable Events: Classify transactions as capital gains or ordinary income and calculate gains/losses using methods like FIFO, LIFO, or HIFO.

- Complete IRS Forms: Use Form 8949 for disposals, Schedule D for gains/losses, and Schedule 1 or C for income, ensuring alignment with Form 1099-DA.

- File by Deadlines: Submit by April 15, 2026, or request an extension (payment deadlines remain April 15).

The IRS is cracking down on unreported crypto gains, with $120 billion uncovered in 2025 alone. Proper documentation and compliance can help you avoid penalties, audits, or criminal charges. Start early, double-check your records, and consider using tax software or professional assistance.

Gather All Transaction Records

Getting your crypto taxes right starts with having complete and well-organized records from every exchange, wallet, and platform you use. Even a single missing transaction can create discrepancies with the IRS, so it's crucial to document every detail carefully.

Document Purchases, Sales, and Trades

For every transaction, make sure to record these key details:

- Date and time of the transaction

- Type of asset (e.g., BTC, ETH, MATIC)

- Quantity of the asset

- Transaction type (buy, sell, or swap)

- Fair Market Value (FMV) in USD at the time of the transaction

- Cost basis, which includes the purchase price plus any fees

- Total proceeds from the transaction

- Fees (exchange commissions, platform fees, blockchain gas fees)

These fees directly impact your taxable gains, so keeping track of them is essential.

"Accurate recordkeeping is essential for calculating your tax correctly." - CA Ankit Agarwal, Head of Tax, KoinX

To stay ahead, download CSV exports, wallet histories, TXIDs, screenshots, and confirmation emails as soon as possible. Many exchanges limit how long transaction histories are available, so aim to download these files at least quarterly. Keep separate records for each wallet or account you use. This level of detail will make it much easier to identify taxable events and calculate your gains or losses when the time comes.

Track Income Events

Crypto income isn't just about trades. You also need to track other types of income events, such as:

- Staking rewards

- Mining payouts

- Airdrops

- Hard forks

- Interest payments

- Compensation for services

For each of these income sources, record the date received and the FMV in USD at the time. If you're running a business, save receipts for any related expenses to back up your deductions.

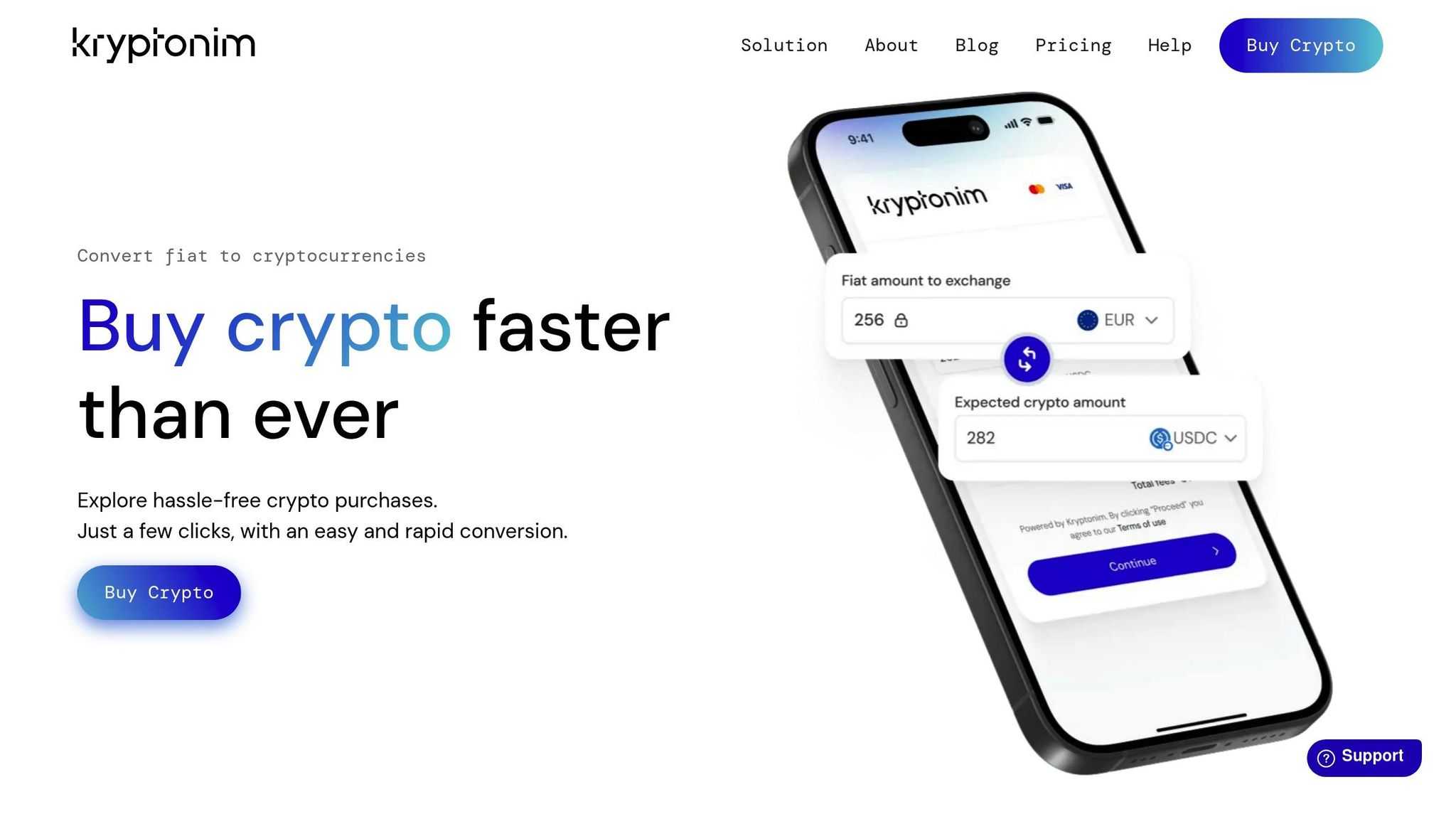

Use Platforms Like Kryptonim for Purchase Records

If you use Kryptonim to purchase crypto, make it a habit to immediately download or screenshot the confirmation. This should include details like:

- Amount spent

- Crypto received

- Exchange rate

- Applicable fee (2% for EU users, 4% for others)

This documentation establishes your cost basis and ensures you're audit-ready, especially since Kryptonim operates under EU regulations. Having these records on hand can save you a lot of hassle down the road.

Identify Taxable Events and Calculate Gains/Losses

Once your cryptocurrency transactions are organized, the next step is to pinpoint taxable events and determine how they impact your tax liability. The IRS views cryptocurrency as property, meaning every sale, trade, or similar transaction can trigger a taxable event. After identifying these events, you’ll calculate your gains and losses using a consistent method.

Classify Taxable Events

Start by dividing your transactions into two categories: capital gains events and ordinary income events.

Capital gains events occur when you dispose of cryptocurrency, such as:

- Selling crypto for USD.

- Swapping one cryptocurrency for another (e.g., trading BTC for ETH).

- Spending crypto on goods or services.

- Converting crypto into stablecoins.

To calculate your capital gain or loss, subtract the cost basis (what you paid for the crypto plus fees) from the proceeds (fair market value at the time of sale, minus transaction costs).

Ordinary income events happen when you earn cryptocurrency. Examples include:

- Mining rewards.

- Staking payouts.

- Airdrops and tokens received from hard forks.

- Interest earned through lending or DeFi platforms.

- Receiving crypto as payment for work or services.

For these events, report the fair market value of the cryptocurrency in USD at the time you received it as income.

Some activities, however, are not taxable. These include:

- Buying cryptocurrency with USD.

- Transferring crypto between your own wallets (excluding fees like gas costs).

- Simply holding crypto.

- Donating crypto to qualified 501(c)(3) charities.

"Virtual currency is treated as property and general tax principles applicable to property transactions apply to transactions using virtual currency." - Internal Revenue Service

To calculate capital gains or losses, use this formula:

Capital Gain or Loss = Proceeds (sale price) – Cost Basis

Remember, holding periods matter. If you hold a cryptocurrency for 12 months or less, gains are taxed at short-term rates (10% to 37%). For assets held longer than a year, long-term capital gains rates apply (typically 0%, 15%, or 20%).

Choose a Calculation Method

After identifying taxable events, select a cost basis calculation method that aligns with your trading history. The IRS allows several methods, and your choice can significantly affect your taxable gains:

- FIFO (First-In, First-Out): This default method assumes you sell your oldest assets first. In a rising market, this often leads to higher gains.

- LIFO (Last-In, First-Out): This method sells your most recent purchases first, potentially reducing gains if those purchases were made at higher prices.

- HIFO (Highest-In, First-Out): This approach prioritizes selling units with the highest purchase price first, minimizing taxable gains.

For example, consider Mark in early 2025. He bought 2 BTC for $20,000 each in January and 1 BTC for $21,000 in March. In May, he sold 2 BTC for $34,000 each. Using FIFO, his cost basis was $20,000 per coin, resulting in a $14,000 gain per BTC.

Now look at Henry, who bought 1 BTC at varying prices in 2025: $15,000 in January, $50,000 in February, and $40,000 in March. When he sold 1 BTC for $15,000 in April, FIFO showed no gain, while LIFO and HIFO recorded losses of $25,000 and $35,000, respectively.

Starting January 1, 2025, the IRS requires you to track cost basis separately for each wallet or account, rather than pooling across your portfolio. This means maintaining individual records for each wallet, including acquisition dates, cost basis, and wallet addresses.

If you want to use methods like LIFO or HIFO, you’ll need detailed records. The IRS has issued Notice 2025-7, providing a grace period through the end of 2025 to use these methods without prior exchange notification - provided your records are accurate and audit-ready.

Prepare Required IRS Forms

To properly report your crypto activities, you'll need to translate your gains, losses, or income into the appropriate IRS forms. With your calculations in hand, it's time to fill out the required paperwork.

Fill Out Form 8949

Form 8949 is where you document every crypto disposal - whether you're selling for USD, trading BTC for ETH, or using crypto to purchase goods. Each transaction gets its own line, divided into two parts: Part I for short-term transactions (held 12 months or less) and Part II for long-term transactions (held more than 12 months).

Starting with the 2025 tax year, the IRS added specific checkboxes for digital assets on Form 8949. These include Box G, H, or I for short-term transactions in Part I and Box J, K, or L for long-term transactions in Part II. Here's how to choose the right box:

- Box G or J: Use these if you received a Form 1099-DA showing that the cost basis was reported to the IRS.

- Box H or K: Use these if you received a 1099-DA, but the cost basis was not reported.

- Box I or L: Use these if you didn’t receive any broker form, which is common for private wallets or decentralized exchanges.

For each transaction, you'll need to fill out the following columns:

- (a) Description of the asset (e.g., "0.5 BTC")

- (b) Date acquired

- (c) Date sold

- (d) Proceeds (fair market value at the time of sale, minus fees)

- (e) Cost basis (purchase price plus any transaction fees)

- (h) Gain or loss from the transaction

After listing all your disposals on Form 8949, transfer the totals to Schedule D (Form 1040). This form summarizes your net capital gain or loss. If you end up with net losses, you can deduct up to $3,000 annually against ordinary income, with any remaining losses carried forward to future tax years. Once this is complete, you’ll need to handle any crypto income separately.

Report Crypto Income

If you earned crypto through activities like staking, airdrops, or hard forks, this income must be reported differently. The fair market value of the crypto in USD at the time you received it determines the amount you report.

- For personal activities (e.g., staking rewards or airdrops), report the income on Schedule 1 (Form 1040), Part 1, Line 8 ("Other Income").

- If your crypto activities qualify as a business (e.g., mining, running a validator, or receiving crypto as freelance payment), report the income on Schedule C (Form 1040). This form also allows you to deduct related expenses like electricity, hardware, or software costs. Note that self-employment tax applies if your net profits are $400 or more.

Starting in 2026 (for the prior tax year), brokers and exchanges will issue Form 1099-DA to report gross proceeds and, in some cases, cost basis. Compare any 1099-DA forms you receive with your own records to ensure accuracy. Additionally, some platforms may send Form 1099-MISC for staking rewards or other income exceeding $600.

Lastly, remember that Form 1040 includes a mandatory yes-or-no question about digital asset activity. If you received, sold, exchanged, or disposed of any digital assets during the year, you must check "Yes" - even if no tax was owed on those transactions.

sbb-itb-0796ce6

Review and File Your Tax Report

2026 Crypto Tax Filing Deadlines and Key Dates

Verify and Double-Check Records

Before filing your taxes, take the time to carefully verify your records. Gather data from all your exchanges, wallets, and DeFi platforms. You can do this by downloading CSV files or using API connections to ensure you haven’t left anything out. If you’ve made external wallet transfers, double-check that the cost basis details are accurate.

It’s also essential to reconcile your records with Form 1099-DA, which brokers started issuing in February 2026. The IRS now uses automated systems to compare this form with your tax return. Any discrepancies could lead to notices or penalties. As highlighted in an analysis:

"The 'they'll never know' era has definitively ended. Prior to 2025, many taxpayers believed cryptocurrency was untraceable... The IRS now has independent verification of your cryptocurrency activity." – MEXC Blog

Ensure that all transaction fees - like gas fees, exchange fees, and withdrawal fees - are either included in your cost basis or deducted from your proceeds. Transfers between your own wallets should be marked as non-taxable, but remember that gas fees associated with these transfers count as taxable disposals. Don’t forget that crypto-to-crypto trades are taxable events and must be recorded as such. Use a consistent method to calculate the fair market value of every transaction in USD at the time it occurred.

Once you’ve resolved any discrepancies and consolidated your records, you’ll be ready to move on to filing.

File Taxes by the Deadline

After verifying your records, file your tax return without delay. The standard federal tax filing deadline is April 15, 2026. If you’re a U.S. citizen living overseas, you have until June 15, 2026 to file. Need more time? You can request an extension by submitting Form 4868, which pushes your filing deadline to October 15, 2026. However, keep in mind that an extension to file does NOT extend the deadline to pay any taxes owed. Payments are still due by April 15 to avoid interest charges.

| Deadline | Category | Requirement |

|---|---|---|

| February 17, 2026 | Broker Reporting | Exchanges issue Form 1099-DA |

| April 15, 2026 | Standard Filing | Submit Form 1040, Schedule D, and Form 8949 |

| June 15, 2026 | U.S. Expats | Filing deadline for citizens living abroad |

| October 15, 2026 | Extension | Final deadline for those filing Form 4868 |

Keep detailed records of your transactions - such as transaction hashes, wallet addresses, and fair market value data - for at least seven years. These records are crucial if you face an audit. The IRS now works with blockchain analytics companies like Chainalysis to trace wallet activity back to individuals. In 2025, the average penalty for significantly underreporting crypto taxes was $43,000, in addition to the taxes owed. If you receive IRS Letters 6173, 6174, or 6174-A, it’s critical to review your records and respond immediately. Letter 6173 is especially serious and requires a formal response to avoid an audit.

Conclusion and Final Tips

Once your records are organized and your gains calculated, it's time to finalize your crypto tax reporting strategy. Start by gathering all transaction records and pinpointing taxable events like sales, swaps, or staking rewards. Use a consistent method to calculate your gains and losses. Then, complete the necessary IRS forms - Form 8949, Schedule D, and Schedule 1 - and don’t forget to answer the digital asset question on Form 1040. Double-check your records against Form 1099-DA, and make sure everything is filed by April 15, 2026.

After filing, consider automating your record-keeping to avoid future errors. Specialized software can help track complex trades and NFT transactions. Many tools connect directly to wallet APIs, consolidating data for each wallet, a feature that aligns with the 2026 IRS requirements. These tools also calculate fair market values for transactions and generate tax forms, saving you time and effort.

For simpler crypto purchases, platforms like Kryptonim offer a secure, EU-regulated solution. They provide transparent pricing with no hidden fees and don’t require account creation, making it easier to manage transaction histories during tax season. With rates of 2% per transaction for EU users and 4% for other regions, Kryptonim helps streamline fiat-to-crypto purchases while keeping tax preparation straightforward.

Finally, keep your records for at least seven years. This includes transaction hashes, wallet addresses, and confirmation emails. Proper organization now can protect you from potential audits and costly mistakes later.

FAQs

What counts as a taxable crypto event?

In the United States, certain cryptocurrency transactions are considered taxable events. These include:

- Selling cryptocurrency for cash: When you convert your crypto assets into U.S. dollars or any other fiat currency, it triggers a taxable event.

- Trading one cryptocurrency for another: Swapping Bitcoin for Ethereum, for example, is also subject to tax reporting.

- Using cryptocurrency to pay for goods or services: Whether you're buying a coffee or paying for a service with crypto, this counts as a taxable event.

Each of these transactions typically requires you to report the details on your taxes.

How do I choose FIFO, LIFO, or HIFO for cost basis?

When deciding between FIFO (First In, First Out), LIFO (Last In, First Out), or HIFO (Highest In, First Out), your choice should reflect your tax strategy. By default, the IRS uses FIFO, but you can switch to LIFO or HIFO with proper documentation.

HIFO can be particularly useful for lowering your tax bill since it prioritizes selling the highest-cost assets first, potentially reducing your taxable gains. Whatever method you choose, ensure it aligns with your financial goals and keep detailed, consistent records to stay compliant.

What should I do if my Form 1099-DA doesn’t match my records?

Discrepancies between Form 1099-DA and your personal records can happen more often than you'd think. These differences usually arise from variations in the data's scope or the methods used to calculate it. Keep in mind that Form 1099-DA reports exchange-level gross proceeds, which might not fully match up with your complete transaction history or reflect your cost basis.

It's essential to identify and explain these differences clearly on your tax return. If you're unsure how to proceed or want to ensure accuracy, reaching out to a tax professional can be a smart move. They can help you navigate the reporting process and avoid potential issues.