Aggregator vs Direct On-Ramp Integration: Trade-offs

Assess aggregators vs direct on‑ramp integrations: coverage, fees, KYC, UX, and when to choose each approach.

If I need to choose fast, I use this rule: an aggregator is better for more countries, more payment methods, and backup routing; a direct integration is better for lower long-term cost, one steady checkout flow, and more product control.

Here’s the short version:

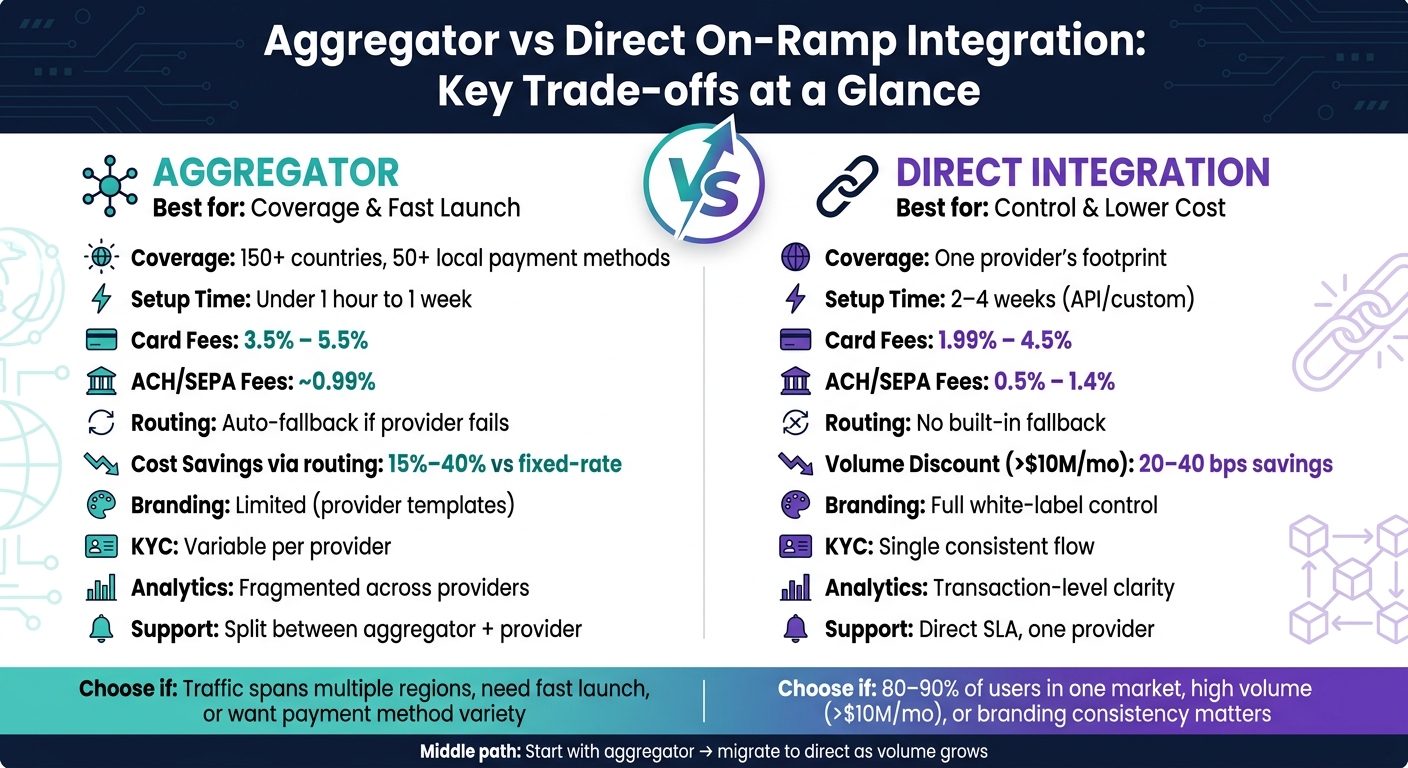

- Aggregators help me launch fast with one API and access to 150+ countries and 50+ local payment methods.

- Direct integrations usually give me lower fees at scale, more control over branding, and one fixed KYC flow.

- Card payments often cost about 3.5%–5.5% with aggregator setups and about 1.99%–4.5% with direct setups.

- ACH or SEPA is usually cheaper, from about 0.5% to 1.4% on direct deals and around 0.99% on some aggregator flows.

- If one provider goes down, an aggregator can often reroute the transaction. With direct, I’m tied to one provider.

So the trade-off is simple: reach vs. control.

If my users are spread across many markets, I’d lean toward an aggregator. If most of my users are in one market and I care about branding, support visibility, and fee predictability, I’d lean toward direct.

Aggregator vs Direct On-Ramp Integration: Key Trade-offs at a Glance

Quick Comparison

| Criteria | Aggregator | Direct Integration |

|---|---|---|

| Setup time | Often under 1 hour to 1 week | Often 2–4 weeks for custom/API work |

| Coverage | Broader country and payment method support | Limited to one provider’s footprint |

| Fees | Usually higher due to markup | Usually lower, especially at volume |

| KYC flow | Can change by provider | One consistent provider flow |

| Reliability | Backup routing across providers | No built-in fallback |

| Brand control | More limited | More control |

| Support | Split across aggregator + provider | One provider, one SLA |

| Best fit | Fast launch, global spread | Core markets, higher volume, tighter UX |

I’d read the rest of this article as a decision guide: pick aggregator for coverage and fallback, pick direct for consistency and cost control.

sbb-itb-0796ce6

How Aggregator On-Ramp Flows Work

When a user enters a crypto amount and a fiat amount, the aggregator checks its provider network and sends the checkout to the best fit. That match is usually based on the lowest total cost or the highest approval rate. In some flows, the user sees a comparison screen and picks a provider. In others, routing happens automatically.

After that, the user completes KYC with the chosen provider, adds payment details like a card, ACH, or SEPA transfer, and the crypto is sent to the user’s wallet - often within minutes. That kind of flexibility can expand reach fast. But it also affects pricing, support, and how consistent the checkout feels from one transaction to the next.

One API or SDK can replace several provider integrations while also expanding country and payment-method coverage.

Fees, Coverage, and Payment Methods

Pricing in an aggregator setup usually includes both provider fees and the aggregator’s markup. Card purchases often fall between 3.5% and 5.5%, while SEPA bank transfers can be as low as 0.99%.

There’s a clear upside here: routing can push prices down because providers compete for each transaction. In practice, that can cut user costs by 15% to 40% compared with using one fixed-rate provider.

The catch is that pricing isn’t always easy to read. Exchange-rate spreads may not be shown clearly, which can add another 0.5% to 1.5% to the effective cost. Lower prices can help conversion. But if users can’t tell what they’re paying, that confusion can add friction at checkout.

User Experience, KYC Friction, and Reliability

One of the biggest day-to-day advantages of an aggregator is fallback routing. If one provider fails, the transaction can be sent to another provider instead. That can keep checkout alive when a single partner has issues.

Still, there’s a trade-off. Because aggregators depend on multiple providers, the checkout flow often ends up being shaped by the weakest provider in the network. One transaction may feel smooth, while the next feels clunky.

KYC can also change from one transaction to another. If a user is routed to a provider they haven’t used before, they may need to verify their identity again - even if they already passed KYC with a different provider. And when a transaction fails, support can get messy because it’s not always obvious where the breakdown happened.

| Feature | Aggregator |

|---|---|

| UX/Branding | Less uniform; constrained by provider templates |

| KYC Friction | Variable; depends on which provider is selected |

| Geographic Coverage | 150+ countries; 50+ local payment methods |

| Uptime Resilience | High; automatic fallback if one provider fails |

| Integration Overhead | Low; one API for multiple providers |

| Fee Transparency | Not always fully transparent; spreads may not be visible |

Direct integrations solve some of these consistency issues by locking the flow to one provider.

How Direct On-Ramp Integration Works

A direct integration connects your app to one on-ramp provider through a hosted widget, an SDK, or a direct API.

Hosted widgets are prebuilt checkout pages or redirects that handle checkout and KYC from start to finish. They’re often the fastest way to go live, sometimes in less than an hour.

SDKs keep users inside your app, which means they can finish a purchase without leaving your product’s environment. That usually feels smoother from a user’s point of view.

Direct APIs give developers the most control. You can build a custom checkout, shape the KYC flow, and fine-tune how the experience works. But that control usually takes weeks of engineering work.

The trade-off is pretty simple: you get consistency, but you give up routing options. There’s also no backup provider built in.

Pricing Control and Long-Term Economics

The biggest upside is cost control.

Card fees usually range from 1.99% to 4.5%, while bank transfers through ACH or SEPA can be as low as 0.5% to 1.4%. Because there’s no aggregator markup, pricing is easier to forecast.

At higher volume, direct deals can get cheaper too. If you’re doing more than $10 million per month, fees can drop by 20 to 40 basis points compared with aggregator models.

Of course, those lower rates don’t just appear out of thin air. You usually need to put in the engineering work first and then negotiate terms.

Branding, Analytics, and Single-Provider Limits

Direct integration also gives you more control over the checkout experience. Providers often support fully branded flows, so the purchase experience can feel like part of your product instead of a handoff to someone else.

There’s also a support angle here. Since all transactions run through one provider, support teams can use transaction-level data and webhooks to investigate failed payments faster under direct SLAs. When something breaks, that kind of visibility matters.

The downside is concentration risk. Your product depends on one provider’s uptime, licensed regions, and payment method coverage. If that provider doesn’t support local payment methods like PIX in Brazil or UPI in India, conversion in those markets can take a hit.

And if the provider goes down, there’s no automatic fallback. The Wyre shutdown in January 2023 made that risk hard to ignore.

| Feature | Direct Integration |

|---|---|

| Cost Control | Negotiable volume discounts; no aggregator markup |

| UX Consistency | Full control over branding and purchase flow |

| KYC Predictability | Single, consistent flow; no fallback if a user fails KYC |

| Support Access | Direct SLAs; transaction-level data available |

| Single-Provider Risk | High; uptime and coverage tied to one provider |

Which Model Fits Your Product and Users

Pick based on launch speed, where your users live, and how much engineering time your team can spare.

Best Fit for Beginners, Apps, and Merchants

The trade-offs above help you match the model to the buyer, the market, and the checkout goal.

First-time buyers usually convert better with a simple checkout, familiar payment methods, and as few steps as possible. That lines up with the KYC predictability and steady UX that come with a direct integration.

Geography changes the picture fast. If 80% to 90% of your users are in one market, a direct integration with strong local coverage is often the cleaner option. If your traffic is split across regions, routing flexibility starts to matter more.

Merchants that care a lot about branding and keeping the whole experience inside checkout often lean toward direct integration. Aggregator-style flows make more sense when local payment methods are the main thing driving conversion in the markets you want to reach.

Where Kryptonim Fits in These Trade-Offs

Kryptonim is an EU-regulated platform built for low-friction crypto purchases. Users can complete a purchase without creating an account, which cuts out one of the biggest drop-off points in a first-time buyer flow.

Its pricing is clear: 2% per transaction for EU users and 4% for users in other regions, with no hidden fees. Kryptonim is a strong fit for teams that want a no-account checkout and simple pricing.

The table below turns these use cases into a quick decision check.

Side-by-Side Summary and Final Takeaways

After weighing fees, coverage, KYC, and reliability, the choice is pretty simple: go with the setup that fits your launch speed, user reach, and fee goal.

Aggregators lean toward broad coverage and fast rollout.

Direct integrations lean toward control and steadier performance.

A lot of teams take the middle path. They start with an aggregator to get live fast, then switch to direct integration in their main markets once volume grows. That approach makes sense. Early on, the main goal is getting the largest share of users to a usable balance. Fee tuning can come after that.

Use the summary below to line up each model with your stage and user base.

Comparison Table and Decision Checklist

| Metric | Aggregator | Direct Integration |

|---|---|---|

| Integration Speed | Under 1 hour to 1 week | 2–4 weeks for an API or custom build |

| Fees | Usually higher | Usually lower at volume |

| Global Coverage | Broader multi-market coverage | Depends on one provider |

| Payment Methods | More local options | Core rails |

| KYC Control | Provider-managed, with possible multiple KYC prompts | Single, reusable flow with stronger data ownership |

| Branding | Standardized widget UI | Full white-label control |

| Reliability | High, with multi-provider redundancy | Depends on one provider's uptime |

| Analytics | More fragmented across providers | Clearer transaction-level data |

| Support Model | Layered across the aggregator and underlying provider | Direct SLA with one provider |

There’s a practical way to read this.

- If your traffic is spread across regions, routing resilience matters more than a small fee gap.

- If most users come from one main market, direct integration usually converts better.

FAQs

How do I decide based on my users’ countries?

Look at where your users are and how they like to pay.

If most of your users are in core markets like the United States, United Kingdom, or European Union, a direct provider is often the better fit.

If your users are spread across many countries, an aggregator usually makes more sense. That’s because it can support local payment methods like PIX or UPI, which can help improve conversion.

When does direct integration become cheaper?

Direct integration gets cheaper as your platform grows, especially when monthly transaction volume goes past $10 million. At that level, direct contracts can skip aggregator markups and cut fees by 20 to 40 basis points.

It also makes more sense when you're focused on one market and a single provider already has strong pricing plus dependable payment rails, like domestic bank transfers.

How much KYC friction should I expect?

It depends on whether you work with a direct provider or an aggregator.

A direct provider usually gives you a steadier experience. In most cases, they offer hosted, prebuilt widgets that handle KYC and AML for you. That takes a lot off your team’s plate and can lower both day-to-day workload and compliance risk.

Aggregators, on the other hand, connect to multiple providers. That can help you reach more users across more markets. But there’s a trade-off: KYC rules may vary more by region, which can make the user journey feel less consistent. Support can get messier too, especially when users drop off in the middle of verification.