Top Challenges in Cross-Border KYC Compliance

Major cross-border KYC hurdles—regulatory divergence, privacy vs AML, and diverse ID checks—and how AI, blockchain, and real-time monitoring can streamline compliance.

Cross-border KYC (Know Your Customer) compliance is a constant struggle for global crypto platforms. Why? Because every country has its own rules, privacy laws often clash with transparency requirements, and ID verification methods differ widely. Here's a quick breakdown:

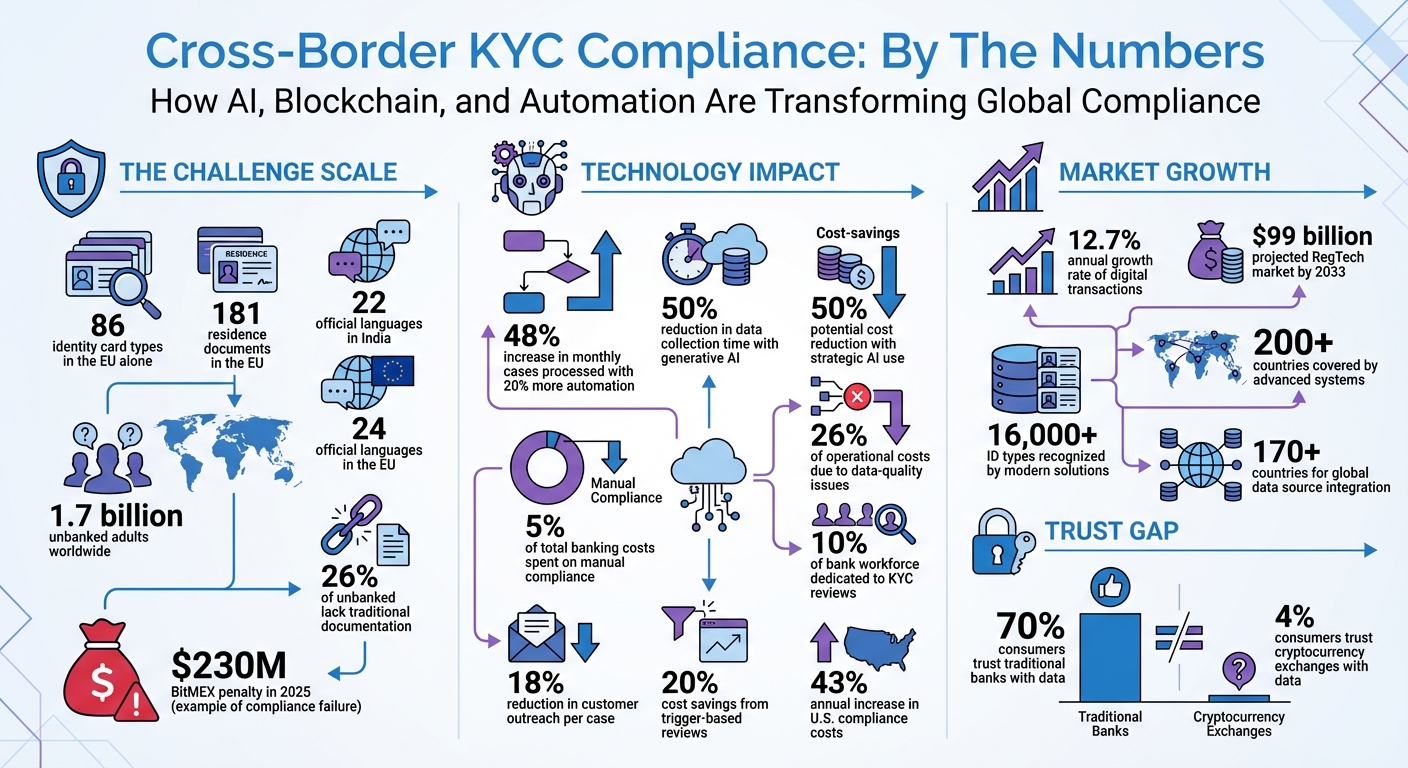

- No universal rules: What's allowed in one country might be restricted in another. For example, the EU alone has 86 identity card types and 181 residence documents.

- Privacy vs. transparency: Laws like GDPR limit data sharing, making it harder to meet Anti-Money Laundering (AML) standards.

- Verification hurdles: Regions with poor tech infrastructure rely on outdated methods, slowing processes.

The stakes are high. A misstep, like BitMEX's $230M penalty in 2025, can lead to massive fines or shutdowns. To tackle these challenges, platforms are turning to AI, blockchain, and real-time monitoring. These tools reduce costs, speed up verification, and improve fraud detection. For example, AI can cut manual compliance costs by up to 50%.

Platforms like Kryptonim are leading the way with solutions like account-free verification and transparent pricing. By combining automation and smart contracts, they simplify compliance while addressing privacy concerns. The future of cross-border KYC lies in smarter tools and better global collaboration.

Cross-Border KYC Compliance Challenges and Solutions Statistics

Main Challenges in Cross-Border KYC Compliance

Crypto platforms face three major hurdles when it comes to cross-border Know Your Customer (KYC) compliance: varying regulations, conflicts between privacy and anti-money laundering (AML) laws, and differences in ID verification methods. These issues not only complicate the onboarding process but also hike up compliance costs. Let's dive into these challenges in more detail.

Different Regulations in Each Country

KYC rules are far from uniform, with each country setting its own standards. The European Union (EU), for instance, presents unique obstacles due to the sheer variety of identity documents and its 24 official languages. In tech-savvy nations, digital KYC processes integrate smoothly with real-time biometric checks. But in regions with weaker technological infrastructure, platforms often have to rely on static images instead of live biometric verification.

Adding to the complexity, risk ratings and document standards vary significantly across countries. The EU's Travel Rule, set to take effect on December 30, 2024, will further challenge compliance by requiring Crypto-Asset Service Providers to identify and handle missing or incomplete information during transfers.

Privacy Laws vs. AML Requirements

Privacy laws and AML regulations often clash, creating a tricky balancing act for compliance teams. While AML rules emphasize transparency and the sharing of information across borders to detect suspicious activities, privacy laws like the General Data Protection Regulation (GDPR) impose strict limitations on data movement. These conflicting demands make it harder to share information effectively.

"Inconsistent national approaches also create obstacles in identifying and verifying customer and beneficial owners, effective screening for targeted financial sanctions, sharing of customer and transaction information where needed, and establishing and maintaining correspondent banking relationships" - FATF

This tug-of-war can make it difficult for financial institutions to verify beneficial owners, especially when local privacy rules restrict access to ownership data. On top of that, differences in how data is formatted across jurisdictions make it even harder to build a unified compliance system.

Inconsistent ID Verification Methods

The variety in ID verification processes across regions adds another layer of complexity. For example, India has 22 official languages, making it challenging to verify local identity documents. In the United Kingdom, the lack of a national identity card program forces platforms to accept a wide range of documents instead.

Modern KYC systems often rely on high-quality images or video for biometric checks, but in areas with poor network connectivity or outdated mobile devices, these processes can become a headache. Even something as basic as address formatting varies widely from one country to another, making automated data extraction more difficult.

To tackle these challenges, platforms need advanced systems capable of handling a vast array of document types. Some modern solutions can recognize over 16,000 ID types from more than 200 countries. Emerging technologies are paving the way for better solutions to these cross-border KYC hurdles, offering hope for more streamlined compliance in the future.

Technology Solutions for Cross-Border KYC

New advancements are reshaping how businesses handle cross-border Know Your Customer (KYC) processes. Technologies like artificial intelligence (AI), blockchain, and real-time monitoring systems are streamlining customer verification, cutting costs, and significantly speeding up what used to be lengthy procedures.

AI and Automation for Faster Processing

AI-powered tools are revolutionizing KYC by drastically reducing both time and expenses. For example, banks that increase their KYC automation by just 20% see a 48% rise in monthly cases processed while cutting down customer outreach needs by 18% per case. Generative AI, in particular, can slash the time analysts spend collecting data by 50%, allowing them to focus on more complex risk evaluations instead of repetitive tasks.

Currently, manual compliance work consumes 5% of total banking costs, but implementing AI strategically can reduce these costs by as much as 50%. AI systems excel at automating tedious tasks like data validation, format checks, and routine communication, enabling human teams to concentrate on higher-risk assessments. This shift also addresses data-quality issues, which are responsible for up to 26% of operational costs.

"Banks that remain in pilot mode will be playing catch-up on both capability and cost." - BCG

The newest AI systems, known as "agentic" AI, go a step further by managing routine client interactions without human input. These systems can handle a variety of document types and adapt to different regulatory requirements across borders. Financial institutions are no longer just automating old processes - they're redesigning workflows to harness AI's full potential. Alongside AI, blockchain technology is emerging as a powerful tool for secure, efficient data sharing.

Blockchain for Secure Information Sharing

Blockchain offers a game-changing solution for KYC by creating shared platforms where financial institutions can securely exchange data. This eliminates the need for customers to repeatedly submit the same documents, addressing inconsistencies in verification processes. Blockchain's distributed ledger system ensures transparency and compliance with privacy laws, while also cutting down redundancies.

The technology enables "collaborative analytics", allowing institutions to share insights while adhering to data protection regulations like GDPR. By creating tamper-proof verification records, blockchain reduces both the time and cost of compliance operations. With KYC reviews often being the most expensive part of financial crime prevention, and 10% of a bank’s workforce typically dedicated to these efforts, the efficiency gains are substantial.

"By getting the key stakeholders to collaborate, we can develop and adopt digital solutions and shared platforms based on consistent regulatory and data standards. It's critical to make this a standard practice across the financial services industry." - Shubhandu Mukherjee, Director, Protiviti

As digital transactions grow at an annual rate of 12.7%, the need for shared platforms becomes even more urgent. These systems can also help address the challenges faced by the 1.7 billion unbanked adults worldwide, 26% of whom lack the traditional documentation needed for manual KYC processes. Success hinges on early collaboration between business teams, regulators, and operations to develop common data models and standards. While blockchain enhances secure data exchange, real-time monitoring strengthens fraud detection and risk management.

Real-Time Monitoring and Fraud Prevention

Real-time monitoring has transformed KYC from a static, once-a-year task into a dynamic process that reacts to real-world risks. These systems trigger immediate reviews when significant events occur, such as a customer initiating transactions in a new country or entering a different business sector. This adaptability is crucial for navigating the varied regulatory landscapes discussed earlier.

By integrating data from anti-money laundering, fraud prevention, and cybersecurity systems, real-time monitoring creates a comprehensive view of customer risk. Machine learning models quickly detect anomalies and efficiently segment customers, improving risk coverage while reducing operational strain. This approach is particularly effective for cross-border compliance, flagging unusual activity that may signal fraud or regulatory breaches.

"Reliable digital ID can make it easier, cheaper and more secure to identify individuals in the financial sector. It can also help with transaction monitoring requirements and minimise weaknesses in human control measures." - FATF

Advanced monitoring systems also identify misuse of digital IDs, catching stolen or compromised credentials before they can cause harm. By combining anti-fraud and compliance efforts, these tools provide a "single, global customer view" that is critical for managing risk across jurisdictions. With U.S. compliance costs rising by approximately 43% annually, trigger-based monitoring offers a smarter, more resource-efficient way to maintain security and compliance.

sbb-itb-0796ce6

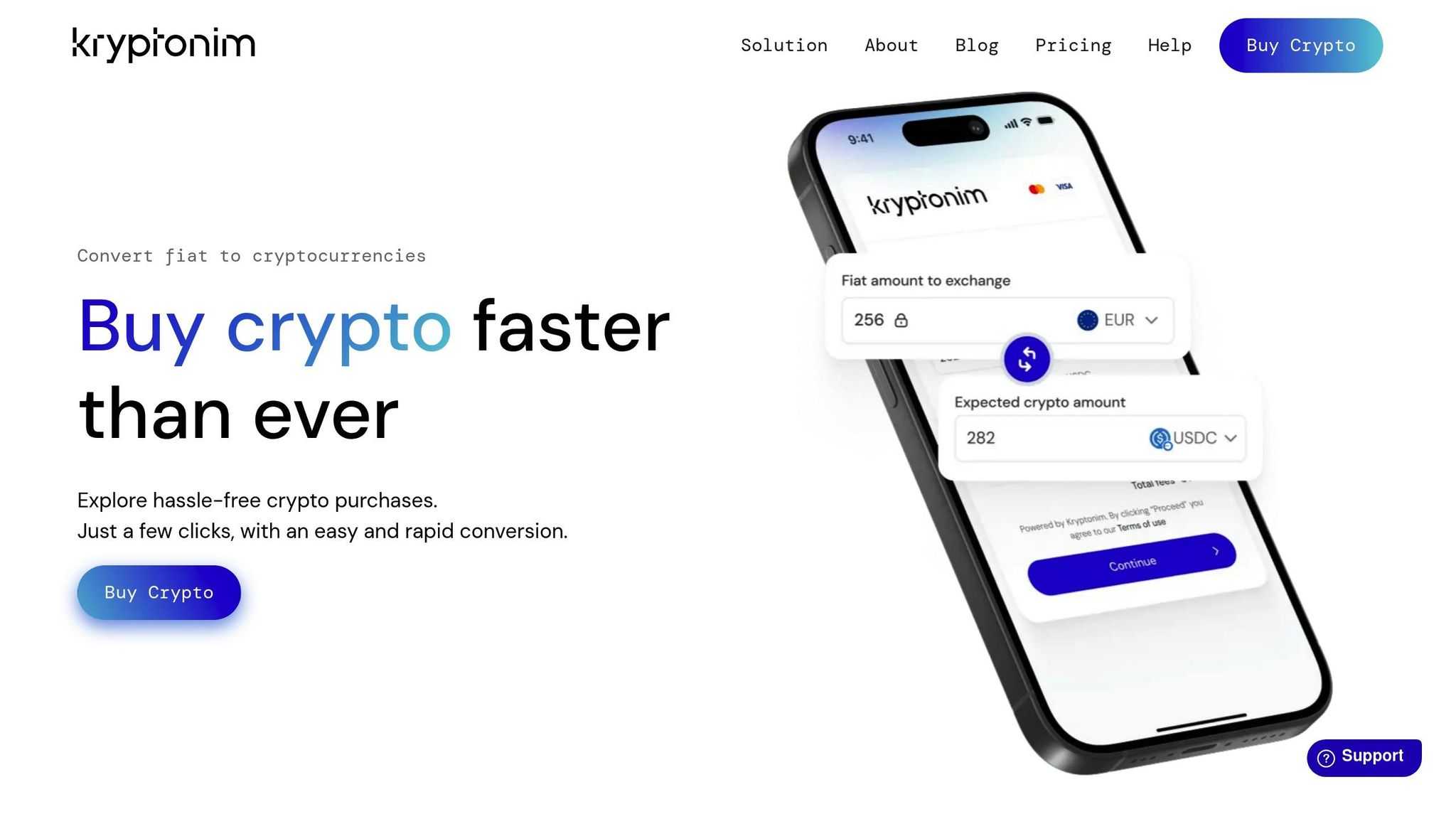

How Kryptonim Handles Cross-Border KYC

Kryptonim operates as an EU-regulated platform under the MiCA framework, ensuring consistent licensing and consumer protection across all member states. By combining automation with smart contracts, the platform tackles one of the toughest cross-border challenges: inconsistent KYC standards. This unified approach simplifies AML (Anti-Money Laundering) and CTF (Counter-Terrorism Financing) compliance across the European Union, creating a more seamless experience for both businesses and users.

To address varying identity standards across EU countries, Kryptonim employs automated smart contracts for verifying customer identities and assessing risk. This reduces errors and speeds up the authentication process. Additionally, AI-driven AML screening works in real time to flag suspicious activities, ensuring compliance without disrupting legitimate transactions. These technological solutions create a strong foundation for modern verification methods.

Verification Without Account Creation

Kryptonim has moved away from traditional account-based verification. Users can complete fiat-to-crypto transactions without creating an account, which means personal data isn’t stored long-term while still meeting regulatory requirements. The platform validates documents and assesses risk in real time, collecting only the essential data needed for compliance.

This method directly addresses privacy concerns by limiting data retention. For users making cross-border transactions, it translates to faster processing without the hassle of repeatedly submitting documents across multiple platforms.

Clear Pricing Structure

Kryptonim simplifies costs by offering a transparent pricing model. EU users pay a 2% transaction fee, while non-EU users face a 4% fee. This clarity eliminates the hidden charges often found in cross-border financial services, such as exchange rate markups or processing fees buried in fine print.

The competitive fees are made possible by the platform’s reliance on automation and smart contracts, which cut down on operational costs compared to manual compliance methods. Users know exactly what they’re paying upfront, making it easier to plan transactions and compare costs across currencies and jurisdictions.

Conclusion

Cross-border KYC remains a challenging task due to fragmented regulations, conflicting privacy laws, and differing verification standards. However, emerging technologies like AI, blockchain, and automated risk assessments are beginning to streamline these processes. For instance, studies show that a 20% boost in automation can increase case throughput by an impressive 48%. These advancements address long-standing issues like inconsistent procedures and rising compliance costs.

Platforms like Kryptonim are stepping up to meet these challenges head-on. By adhering to EU-wide MiCA regulations, offering account-free verification, and maintaining transparent pricing, Kryptonim leverages blockchain technology and AI-driven screening to uphold strict AML standards. This approach also prioritizes user privacy - a critical factor in a market where 70% of consumers trust traditional banks with their data, compared to just 4% who trust cryptocurrency exchanges.

Businesses developing cross-border KYC frameworks can also benefit from refining their strategies. Adjusting verification intensity based on customer profiles and shifting from calendar-based reviews to trigger-based updates can cut operating costs by around 20%. Additionally, integrating global data sources from over 170 countries enables near-instant verification without sacrificing security. These tailored approaches are essential for maintaining compliance on a global scale.

"Through strategic use of AI technologies - including predictive, generative, and agentic AI - banks are targeting cost reductions of up to 50%, streamlining processes, and enhancing compliance and customer experiences." – BCG

While automation can handle routine tasks, high-risk cases and emerging fraud techniques still require the expertise of compliance teams. With the RegTech market expected to hit $99 billion by 2033, businesses that invest in standardized global policies and intelligent automation will be better equipped to navigate the complexities of cross-border compliance. The right balance of automation and human oversight will be crucial for achieving sustainable and effective KYC processes.

FAQs

How do privacy laws like GDPR impact cross-border KYC compliance?

Privacy laws, such as the General Data Protection Regulation (GDPR), play a major role in shaping how businesses manage cross-border KYC processes. GDPR imposes strict guidelines on transferring personal data outside the European Economic Area (EEA). Companies must ensure that the receiving country offers a comparable level of data protection, often relying on legal frameworks like standard contractual clauses, binding corporate rules, or specific exceptions to stay compliant.

For businesses handling cross-border KYC, adhering to GDPR means adopting robust safeguards. This could include localized data storage, encryption, or anonymizing sensitive customer information. These strategies help protect personal data while fulfilling both KYC obligations and GDPR requirements. Platforms like Kryptonim must implement such measures to securely onboard EU-based users without compromising compliance.

How does AI improve KYC processes for cryptocurrency platforms?

Artificial intelligence (AI) is changing the game for KYC (Know Your Customer) processes in the cryptocurrency world. Tasks like document verification, facial recognition, and sanctions screening - once time-consuming and prone to human error - are now automated, cutting onboarding times from days or weeks to just minutes.

Take platforms like Kryptonim, for example. AI enables them to instantly verify IDs, cross-check global watchlists, and flag suspicious activity, all while staying compliant with strict U.S. and EU AML/KYC regulations. This approach not only trims compliance costs but also boosts transparency, fostering trust among users and regulators alike.

With AI in the mix, KYC is no longer a clunky, paperwork-heavy process. Instead, it becomes a dynamic, real-time system that safeguards platforms and users while maintaining speed and convenience.

How does blockchain improve security and efficiency in KYC processes?

Blockchain brings a new level of security and efficiency to KYC processes by using a decentralized, tamper-proof ledger to track identity-related transactions. This setup guarantees data integrity and makes it nearly impossible for records to be altered without detection, significantly reducing the risk of fraud or manipulation.

What’s more, blockchain enables real-time data sharing across borders. Regulators and financial institutions can access a single, trustworthy source of information, cutting down on repetitive identity checks. This not only lowers compliance costs but also speeds up verification processes. And thanks to advanced cryptographic techniques, privacy remains intact throughout.

Take Kryptonim, for example. This platform uses blockchain to offer secure fiat-to-crypto transactions while adhering to EU regulations. It ensures a smooth, compliant experience for users in the U.S., bridging regulatory requirements with user convenience.